AGENDA

- Be A Trusted Advisor

- HECM As A Retirement Tool

- Case Studies

- HECM LOC vs. Traditional LOC

H4P

H4P- HECM Facts

- Marketing through positive press

- Q & A

H4P

H4PDon’t Assume

Don’t assume financial professionals know what may seem obvious to you.

Remember you’re their trusted advisor for the HECM product. Some financial advisors still have the same myths and misconceptions that borrowers do.

- The bank will own your home

- Children will be responsible for the debt

- Homeowners will have to leave if he or she runs out of money.

In the past, reverse mortgages have been viewed as a lifeline or last resort for seniors who are house-rich and cash poor. In fact, this product allows our seniors to have a more secure retirement. This product is a retirement tool and should always be referenced as one.

Food For Thought…

Conversation starters, speaking the advisor’s language.

- Used as a retirement planning tool, a HECM can serve as a standby line of credit that can be an alternative to tapping into investment portfolios.

- A HECM can be used in a down market to improve the chances that a client will not out live their money.

This is what keeps financial advisors up at night!

- A HECM is another way for your clients to address their retirement income needs.

DID YOU EVER THINK OF USING A HECM?

To Fund Long-Term Care

A HECM can be used to fund long-term care (if needed) instead of paying the premiums on long-term care insurance out of pocket that your client may never use.

Using a HECM LOC for your clients may be a solution. Your clients can draw on the LOC when they have in-home health care expenses. The unused funds in LOC grows over time and your only paying interest on the funds used.

Scenario: No Long Term Care Insurance

Situation: 62 year-old couple, home value $500,000 in the state of California. They have a modest investment portfolio and Social Security and no LTCI.

Solution: $256,000 HECM Credit Line that grows to $468,000 in year 10 and $855,000 in year 20).

Result: Clients have a safety net accessible for in-home health care needs

Note: Projections were calculated using MoneyGuidePro and Tango as of September 2015. Examples are provided for illustrative purposes; other terms and conditions would apply

To Defer Social Security Benefits

Situation: Client may need income when they retire at 62, but are hesitant to draw on SS.

Solution: Use the HECM as a tool to provide the same monthly income they would receive from Social Security.

- Retirement benefits at 70 are now 76% larger benefits than at 62.

Do you know about Spousal Benefits?

Spousal benefit at 66 are now 43% larger that at 62

Widow(er) benefit at 66 are now 40% larger than at 60

To Refinance the Home with Cash Out

Scenario: A 66 and 68 year old couple were drawing 10-12% annually from their $500,000 IRA. Part of their excessive withdrawals was due in part to their $2,000 monthly mortgage payment. The financial advisor was alarmed by their withdrawal rate and was searching for ways to reduce it and the resulting taxes so they can preserve their savings for as many years as possible.

Solution: Use a HECM to refinance their mortgage so that they can:

- Eliminate the $2,000 monthly mortgage principal and interest payment. **

- Reduce their savings withdrawal rate.

- Lower the amount of taxes they pay from IRA withdrawals or other investments.**

Borrower is responsible for property taxes, homeowners’ insurance, and property maintenance. A HECM is home-secured debt payable upon default or a maturity event.

**Consult a tax professional

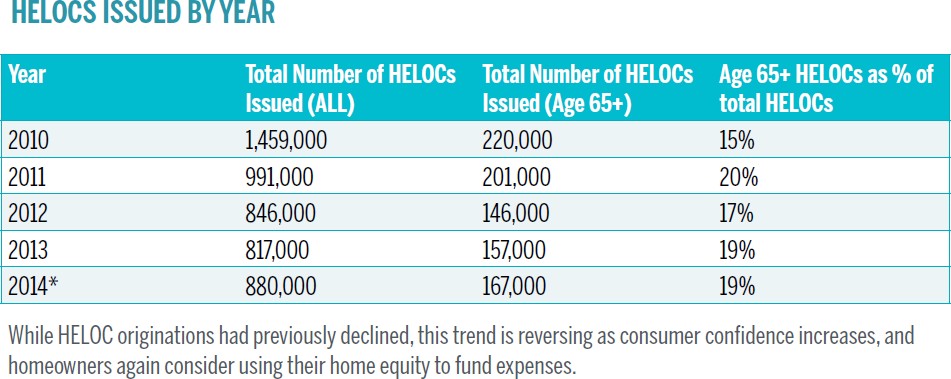

FACTS ABOUT HELOCS

HECM LOC vs. HELOC

Clients have the option to make monthly payments, with no prepayment penalty.

| HELOC | HECM LOC | |

| Line growth? | No | Yes |

| Cancelable? | Yes | No |

| Requires repayment? | Yes | No |

| Age restriction? | None | 62 |

Source: MRI 2013 Doublebase.

FACTS ABOUT HECMs

HECM Facts

- Due and payable when the last borrower (or protected NBS) permanently leaves the home.

- Allows older homeowners to convert a portion of their home’s equity into income tax free *.

- Monthly principal and interest payments not required. ***

- Taxes and insurance paid directly by the borrower or via set-aside.

- All borrowers must be 62 and a citizen or a legal resident.

- All borrowers must be on the deed (some exceptions for Life Estates or Trusts)

- Owner occupied, primary residences

- Borrower(s) retain full ownership in the home.

- Capacity and willingness analysis

** Other maturity or default events are possible.

*** Consult a tax professional

*** Borrower is responsible for property taxes, homeowners insurance, and property maintenance. A HECM is home-secured debt payable upon default or a maturity event.

Property & Financial Requirements

Eligible Property Types

- Single family

- 2-4 units, as long as one unit is the borrower’s primary residence (refi only)

- Manufactured homes

- PUDs

- FHA Approved condominiums

Financial Requirements

- Residual income requirements based on HUD guidelines

- Satisfactory credit based on HUD guidelines

- Timely payment of property charges

Payment Options

- Lump Sum – Draw all the available funds at Closing. The only option available on fixed rate loans.

- Line of Credit – Payments when the borrower requests a disbursement as long as there is an available LOC. The used balance grows over time.

- Tenure – Equal monthly payments for as long as the borrower occupies the property as his or her primary residence

- Term – Equal monthly payments over a fixed period of time

- Modified Tenure or Term – Same characteristics as the term or tenure plan above adding a line of credit feature

*HECMs cannot be called or cancelled as long as requirements are met.

HECM For Purchase (H4P)

Purchase the home you hope for – and conserve cash

The H4P eliminates the need to make regular monthly principal and interest payments. Buyers who opt for an H4P can retain funds for retirement and cash flow.

Scenario: 62 year-old couple sells home for $500,000 and purchases a smaller home in a 55+ community for $425,000. They have a $600,000 investment portfolio and need more guaranteed income.

Solution*: Instead of paying all cash, clients pay $211,322 in cash and uses $213,678 from HECM proceeds to finance the new home closer to their children and grandchildren. Clients make no principal and interest payment.

Note: H4P buyers remain responsible for property taxes, homeowners insurance, and property maintenance. Similar to traditional mortgage buyers.

Clients (and advisor) use extra $213K to generate over $1,000 in guaranteed income.

2X the Purchase Power with HECM For Purchase

In the first example, a homeowner age 62 has an additional $137,479

($275,000 minus $137,521) in buying power by using H4P.

PROVIDING VALUE TO YOUR FINANCIAL ADVISORS

Show the Value of a Reverse Mortgage to the Financial Advisor?

In order to maintain long lasting relationships educate advisors on the potential benefits of a reverse mortgage and how their client’s can use it.

Knowledge is Power- Educate your advisors on why a HECM can be a valuable tool for their client’s retirement plan. Provide examples of how the product can be used as a retirement tool.

- Due to increasing life expectancies, many seniors are running into the problem of outlasting their savings.

- Adding home equity through a reverse mortgage may help to ensure the success of your retirement plan

Provide Industry Related News

GENERAL NEWS

Forbes – Reverse Mortgages Can Be A Retiree’s Saving Grace-

Houston Chronicle – Creativity can grow nest egg after 55-

http://www.chron.com/homes/senior_living/article/Creativity-can-grow-nest-egg-after-55-6569370.php

Main Street – Boosting Retirement Income: How to Generate Funds in Your Golden Years- https://www.mainstreet.com/article/boosting-retirement-income-how-to-generate-funds-in-your-golden-years

NewView Advisors – HREMIC Issuance 2015 First 9 months – Already in the Record Books

Now It Counts Magazine – Can You Use A Reverse Mortgage For Home Remodel? http://nowitcounts.com/can-you-use-a-reverse-mortgage-for-home-remodel/

Reverse Review – Spotlight: The Market is Changing: Advertising Reverse Mortgages in Today’s World http://www.reversereview.com/magazine/spotlight/spotlight-the-market-is-changing-advertising-reverse-mortgages-in-todays-world.html

Reverse Review – Originating: Investing in Retirement, Not Home Purchases

Reverse Review – Feature: The New Retirement Picture http://www.reversereview.com/magazine/features/feature-the-new-retirement-picture.html

Reverse Mortgage Daily – Reverse Mortgages Offer Forward Brokers New Opportunities http://reversemortgagedaily.com/2015/10/12/reverse-mortgages-offer-forward-brokers-new-opportunities/

Reverse Mortgage Daily – Improved ‘HECM 3.0’ Reverse Mortgage Offers Attractive Value to Banks

Reverse Mortgage Daily – Standby Reverse Mortgage Line of Credit: A Retirement ‘Must Have’ http://reversemortgagedaily.com/2015/10/14/standby-reverse-mortgage-line-of-credit-a-retirement-must-have/

HECM For The Financial Professional

Create a binder that you take with you on face-to-face appointments:

- Your Bio

- HECM Fact Sheet

- The organizations that you Network in and Support

- Case studies

- Positive press releases/articles relating to the HECM product

- Financial advisor testimonials on your service and how this product has helped their client.

- Client Testimonials